Mote Money: a mote of dust suspended in a sunbeam

“Mote” means a tiny piece of substance. I chose to include “Pale Blue Dot” as it inspired the famous American scientist, Carl Sagan to write “Look again at that dot. That’s here. That’s home…The history of our species lived there on a mote of dust suspended in a sunbeam.” [7] The sheer size of space puts our planetary existence in perspective on the one hand, but on the other, we have created such a complex history on our small mote of land. Our mote is parva sed potens, Latin for small but powerful. Similar to Carl’s labeling of our home, I’ve labeled my new venture Mote Money, which is a free service that helps Americans get the most out of their credit cards. Mote Money is addressing the question that is often muttered when checking out- what card should I use to get the most out of this purchase?

When checking out online, Mote Money suggests tiny shifts in one’s credit decision-making. Over time, savings generated from these shifts can provide significant value, adding up to thousands of dollars in savings over the course of a year. Like our planetary home, Mote Money is parva sed potens.

This past year saw me rather obsessed, not with interstellar pursuits, but with credit cards and the checkout page. With the world shifting much of their shopping online, both credit cards and the online checkout page became even more ingrained in our daily rituals. Credit cards are one of the primary methods Americans pay for their e-commerce goods. As the facilitator of the exchange of capital and goods, the checkout page is one of the most valuable destinations on the internet.

Services that either streamline checkout or provide more ways to pay online are needed now more than ever. E-commerce growth has rocketed up 44% year over year, yet cart abandonment rates remain stubbornly at 88%. [1] [2] Companies have stepped in to fill those gaps. Buy Now Pay Later (BNPL) lending companies like Affirm, Afterpay, and Klarna are engaged in a land grab to sign up merchants. Payment juggernaut Paypal has created a service helping consumers who had previously been hoarding credit card rewards points for travel to use them to pay for goods and services. In addition, innovative processing companies like Fast.co (backed by Stripe), are looking to turn a lengthy checkout process into a one-click experience. Solutions like these will undoubtedly improve the transaction process at the point of sale, and be a net positive for consumers, merchants, and providers. Despite these emerging options, there is one service that is missing.

Established payment methods still dominate our wallets, including credit cards. Americans’ relationship with credit cards is complicated, but nearly all of us seem to have one. According to Experian, 90% of adults have a credit card account listed in their credit report.[3] Collectively we are just shy of $1 trillion in outstanding debt on 497 million cards.[4] Despite their ubiquity, choosing the best card to use at checkout can be a complex decision. The average American has 3 cards and for each purchase, there are changing rewards, interest rates, cashback offers, and fees to consider.[5] As Mario Gabriele, editor at one of my favorite publications, The Generalist, points out, “Humans are ineffective at snuffling out weird arbitrages across an expanse of changing financial offerings, at least when compared to software.”[6] Most consumers manage their cards through memory, and often, consumers wind up with an unsatisfactory outcome.

Is this something where credit card companies could step in to help? Unlikely. Credit card companies are incentivized to keep things confusing. Between interest fees and late fees, credit card companies pull in nearly $150 billion in revenue each year.

I experienced this conflict of interest between consumers and card issuers firsthand. In 2019, on a new card with a major issuer, I generated a $759 interest fee on my first bill, all because bill alerts were not available. Bill alerts. It is a feature that seems so foundational to a positive credit card experience. While staring at the unnecessary fee on my bill it became evident that an independent service to support consumers with their credit cards was worth pursuing.

In 2007 Ken Lin, founder of Credit Karma (acquired by Intuit, 2020), had the wild idea to give every American access to their credit score for free. Today, 100 million Americans access their score through Ken’s service. In that same spirit, a new service is needed to take the guesswork out of managing credit. The service should be a smart virtual wallet for a consumer’s credit cards and in using it, consumers should have more confidence knowing that they are making smart decisions with their cards every time they shop. Further, providing this decision, at the very point when consumers are about to execute a transaction is not only possible but essential.

The desire to get more out of one’s purchase has emerged in different forms over the last decade. Companies like Wallaby (founded by Matt Goldman and acquired by Bankrate, 2016) established consumers' desire for a better experience with their credit. Coupon companies such as Honey (founded by Ryan Hudson and acquired by Paypal, 2020) elevated the shopping experience through coupon aggregations and showed the world that a $100 million business could be built on a browser extension. I am humbled to be standing on the shoulders of these pioneering entrepreneurs in order to bring a new service to market.

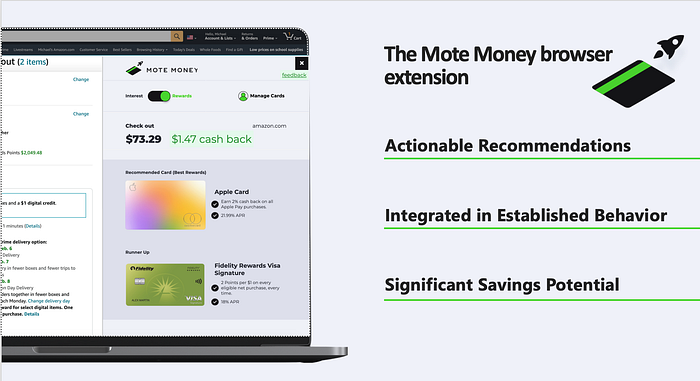

Mote Money is changing the way Americans pay by delivering access to personalized credit card decisioning at the point of sale. Every transaction is an opportunity for credit card owners to maximize rewards or minimize their interest fees. Mote Money also has the ability to propose new credit options based on purchase history and goals.

Mote Money is a browser extension and will work for all online purchases. Users have the ability to manage their card recommendations based on their goals. Users simply shop online and when they are ready to check out, Mote Money’s algorithms will recommend the best card to use. In addition to personalization capabilities, Mote Money avoids collecting passwords, login, or credit card account information, creating an all-around streamlined and secure experience.

The response I get the most when sharing Mote Money is “I get it. Good idea. I could use that with my credit cards.”This feedback is energizing and has helped me bring Mote Money to life. It is my hope that everyone experiences the power of Mote Money. Now that it is here please try it out, share your feedback and start saving!

[1] https://www.digitalcommerce360.com/article/us-ecommerce-sales/

[2] https://www.statista.com/statistics/457078/category-cart-abandonment-rate-worldwide/

[3] https://www.experian.com/blogs/ask-experian/consumer-credit-review/

[4] https://www.federalreserve.gov/releases/g19/current/default.htm

[5] https://www.experian.com/blogs/ask-experian/consumer-credit-review/

[6] https://rfs100.substack.com/p/100-startup-ideas

[7] Carl Sagan, Pale Blue Dot: A Vision of the Human Future in Space